Basic instruments for corporate wealth and economic management

Balance sheet and PyG account

4.1 Financial Reporting Outlook

From an internal perspective:

The Coach should direct his client to make decisions that correct weaknesses that can threaten their future and take advantage of the strengths to achieve their goals

From an external perspective:

These techniques are very useful for all agents interested in knowing the situation and foreseeable evolution of the company, such as:

- Banks

- Shareholders

- Suppliers

- Customers

- Employees, business committees and trade unions

- Account auditors

- Advisors

- Financial analysts

- Public Administration

- Competitors

- Investors and potential buyers of the company

All these agents want to know the reality of the company, of all companies, and for this it is necessary that there is a common language such as Accounting and public information rules such as the obligation to deposit in the Commercial Register the Annual Accounts.

ACTIVITY

The coach together with the entrepreneur will make a list of the reasons why each agent from the previous list is interested in the accounting information of his company/project

4.2 Business analysis and diagnosis

The Coach together with his client must make the diagnosis of the company that is the consequence of the analysis of all the relevant data of the same and informs of its strengths and weaknesses.

To make the diagnosis useful:

- It should be based on the analysis of all relevant data

- It must be done on time

- It’s got to be right.

- It must be accompanied immediately by measures

If the above does not happen we are faced with a situation of incompetence, and you can see some of the following manifestations:

NOT DIAGNOSED

- Companies that decide investments or financial policy, regardless of their situation and PEF

- Companies that sell on credit without analyzing their risk

- Investors who buy shares if they see the annual accounts

- Employees who join a new company without analyzing their annual accounts

WRONG DIAGNOSTICS

- For lack of data, they usually exist, but day-to-day masks

CORRECT DIAGNOSES, BUT LATE

- Delayed accounts

- Poorly carried and unreliable accounts

- Unaudited accounts (officially or not)

CORRECT AND TIMELY DIAGNOSTICS, LATE AND/OR INADEQUATE MEASURES

- Measures that are fled forward

- Protective measures of managers

- Fear of trauma and conflict

Diagnosis is a key (not the only) tool for the correct management of the company and to achieve the objectives of most companies:

ACTIVITY

The participant must:

1.- Search for examples of the diagnoses cited

2.- Reflect on what type of diagnosis the quotes may be more likely to fall due to their way of being.

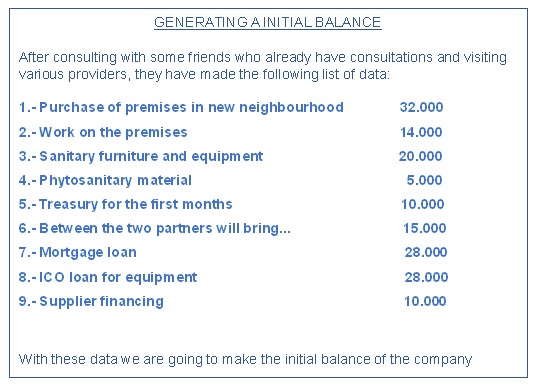

4.3 Building a balance sheet

ACTIVITY

From the following case, the Coach must help the participant build two columns:

- What I need for the business

- How to finance it

ACTIVITY

The client must make their own initial balance, putting in two columns:

- The goods and services you think will need and value approximately

- The amounts you initially estimate you can contribute and what you can get from third parties

This balance should be approximate at the moment of the module, it is advisable to review it at the end of the module

4.4 The Balance sheet and profit and loss account

From the document made for the project, the Coach must achieve a conceptual understanding of the Balance and the chart of accounts.

The graphs below summarize the information that participants should assimilate

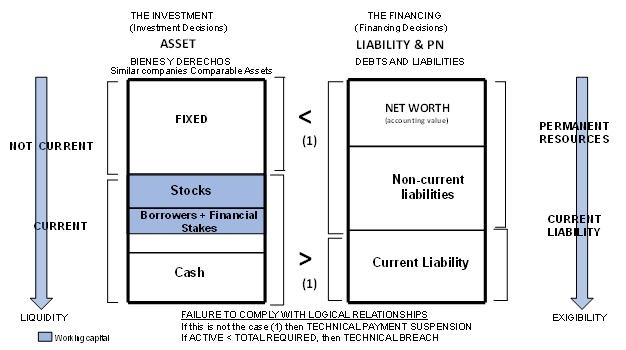

When we talk about balance, we need to understand Balance Sheet, that is, the one that represents the process

accountant at any given time.

From a legal point of view, it represents:

- – Assets and rights in favour of the company (Active)

- – Obligations incurred (Liabilities)

and as a difference, the net worth belonging to the owners

From an economic point of view, it represents:

- Sources of Financing (Liability and Equity)

- Investment or implementation given to such financing (Active)

The Balance among others provides us with the following information:

- Liquidity

- Solvency

- Borrowing capacity

In the Balance sheet we know the economic and financial situation of the company in relation to:

- – What the company owns ASSET

- – What the company owes LIABILITY

- – What you owe the company ASSET

- – Who finances the company LIABILITY & PN

- – How does the company use this funding? ASSET

In short, we can evaluate:

- Liquidity/solvency situation, can payments be met in the short and long term?

- Indebtedness, Is it correct in terms of quality and quantity?

- Warranty, do you have sufficient financial guarantees against third parties?

- Capitalization, is it sufficiently capitalized? Is the ratio of equity to debt correct?

- Asset Management, Is It efficient?

- Financial balance, is the balance sheet balanced from a wealth and financial point of view?

ACTIVITY

Once the basic concepts have been understood and simple exercises on balance sheet charts of companies from different sectors and in different situations of imbalance have been carried out, the participant should

- Draw the balance of your activity and draw your first conclusions.

- Search on the Internet for the financial statements of a company like the one you intend to start and study its balance sheet analyzing the differences with the one made by it

It follows from the above that comparison with the competition can be greatly beneficial, but where do you get the data?

- One way is to go to the Commercial Registry and ask for the accounts of the companies that interest us. This information can be obtained both from the Register’s website and from other websites that provide more elaborate and complete information

- – Another way to compare with the averages of the sector to which we belong, a good source is the annual publication of the Central Balance Sheet Data Office of the Banco of the Country

ACTIVITY:

We analyze the following balance sheet by wealth masses:

| ASSETS | Euros | % | PN & LIABILITY | Euros | % |

| NON-CURRENT ASSET | 57.478 | 51,96% | NET WORTH | 196 | 0,18% |

| Stock | 45.667 | 41,28% | NON-CURRENT LIABILITY | 94.856 | 85,75% |

| Realizable | 6.696 | 6,05% | CURRENT LIABILITY | 15.572 | 14,08% |

| Available | 783 | 0,71% | |||

| Total | 110.624 | 100% | Total | 110.624 | 100% |

We watch.

- The company is undercapitalized (no equity and fully indebted (mostly long-term)

- The current asset made up of virtually stocks

The available and realizable amounts are lower than the current liabilities, so liquidity pressures may arise

Possible measures:

- – Increase capital stock to reduce liabilities

- – Increasing profits and reinvesting them

- – Reduce current liabilities

- – Expedite the completion of stocks in finished products and sell them to increase realizable and available.

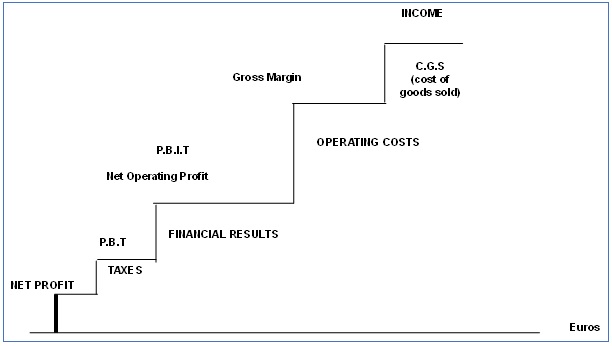

P&L Account

In the Profit and Loss Account we know:

- If the company has made a profit or loss

- How much those profits or losses amount to

- Where those benefits or losses come from

The Profit statement shows what the profit or loss recorded in an entity has been, over a period.

- Evolution of global sales figures by product or business

- Evolution of global gross margin and by products or businesses

- Evolution of structure and financing costs

- Calculating sales to reach the profitability threshold and to achieve economic viability

- Similarly, for forecast accounts

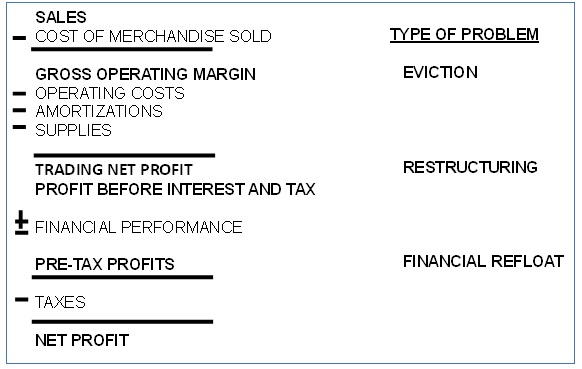

Conceptually the Coach must make the client understand the P&L account in the form of a ladder and the “normality” that the different steps must have

- A company that already has losses in its Gross Operating Margin is at a level of EVICTION, because the more you sell the more you lose.

- A company whose jump is very high from the Gross margin to Net Operating Profit or that the latter is negative indicates that it has excessive operating expenses, that is, is poorly sized and therefore can still have a solution if the company is resized (Template, investments…), that is, we are in a restructuring phase

- If we go from a remarkable or normal PBIT to a negative or small PBT, it will be due to excessive financial expenses due to an extremely high EXIGIBLE in relation to the total LIABILITIES. This company is in a level of FINANCIAL REFLOATMENT, if it manages to change Exigible for own resources (which do not cause financial expenses) it will resume the path of profits.

The P&L account as a management tool

Through case studies, the customer must understand the importance of:

- Get Regularly Profitability Analysis (monthly or quarterly)

- Compare month and cumulative with forecast income statement

- Get Profitability Analysis by Business Areas and/or Projects

ACTIVITY

It is at this time that the participant will begin work with the document:

ANNEX II

It is the role of the Coach to decide the process and timing of the business plan